When most people hear “cashflow modelling,” they picture charts and guesses.

This is fair, but when done correctly, cashflow modelling is a decision tool to rehearse big life choices before making them. Here are seven decisions it helps with, plus three sample timelines to demonstrate how it works (no product or rate specifics).

1) “When can I comfortably work less, or stop altogether?”

Your plan outlines the transition from full-time work to part-time work, sabbatical, or full retirement. We test what-if dates, the impact of completing a mortgage, and the point at which guaranteed incomes begin. The aim is to find the earliest date you can change gears without risking your future lifestyle.

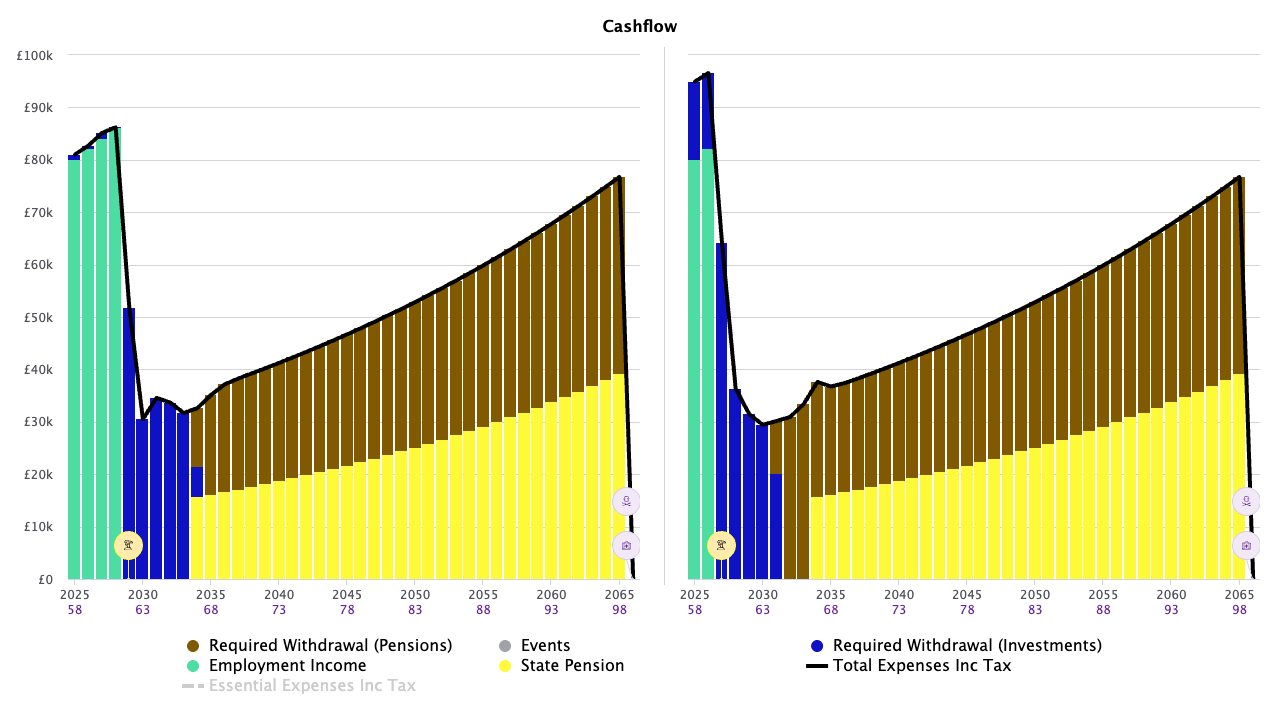

Here is the cash flow chart:

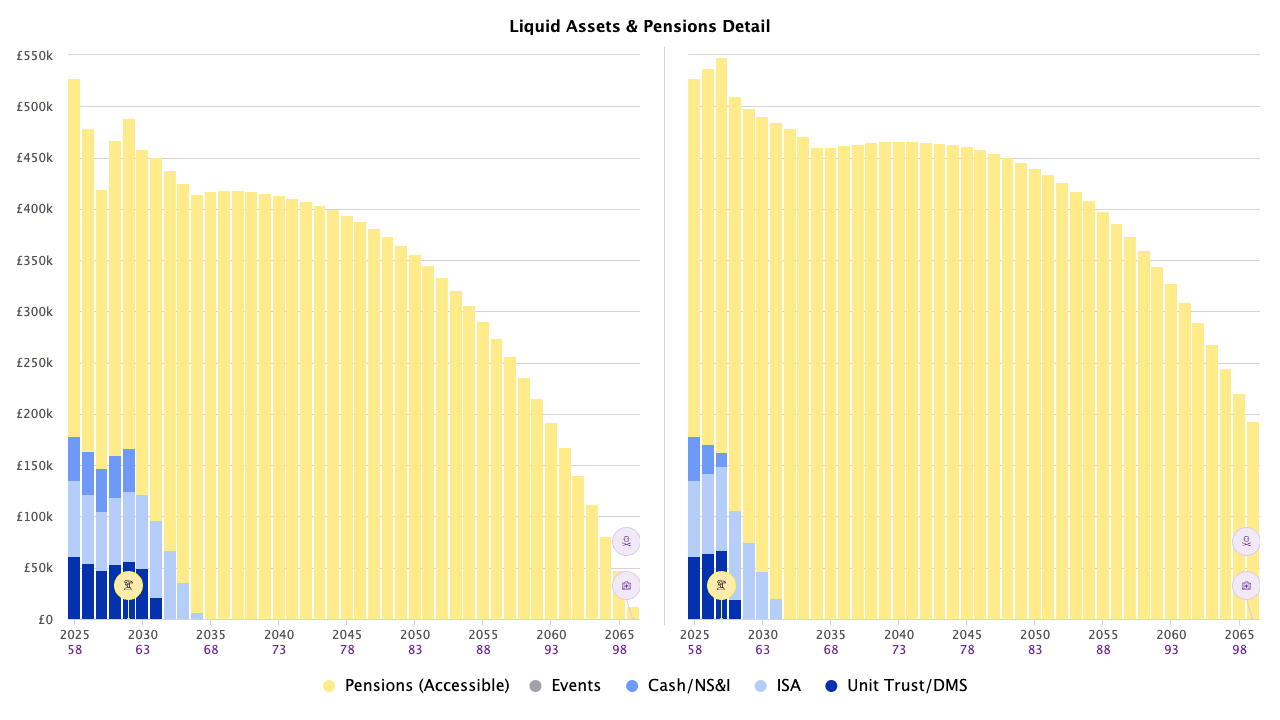

And here is the liquid assets chart

The gap between the base plan and the finish-earlier plan allows you to judge the trade-off.

2) “How much can we safely spend, now vs later?”

We’ll map your required spending (mortgage, bills, essentials) and your discretionary spending (holidays, gifts, hobbies). Then we test different spending profiles, front-loaded, even, or flexible, so you can enjoy more now without compromising later.

Spending isn’t one number forever. It changes as your life changes. The model allows you to adjust it with confidence.

3) “What if life takes a turn?”

Career break, business sale, moving house, caring responsibilities, real life rarely runs in a straight line. The model makes it easy to test what-ifs:

“What if we move and free up equity?”

“What if we take a year out with the kids?”

“What if I change sector and earn less for a while?”

The output isn’t a prediction; it’s a map of options and the least-regret route.

4) “How resilient is our plan to bad market years?”

Two families with similar averages can end up differently due to when bad years hit (known as “sequence risk”). We test your plan against early declines and slow recoveries.

Here is the cashflow chart

And here is the liquid assets chart

The primary difference between the two plans is the buffer we need to add to enhance the plan’s survivability against market downturns in the early years.

5) “How much can we gift without worrying we’ll run out?”

Helping children with a first home, school fees for grandchildren, or giving to causes you care about, generosity is easier when the numbers show you can afford it. We’ll set a safety floor (the level of assets you never want to drop below) and test different gifting schedules against it.

Below is the chart:

6) “How do we line up big one-offs without stress?”

Renovations, replacing a car, a once-in-a-lifetime trip, or a sabbatical: we slot big one-offs into your timeline and show their ripple effects. You’ll see:

- The best year to do it.

- Whether splitting the cost (e.g., over two tax years) smooths the plan.

- How to offset the cost with temporary trims elsewhere.

7) “What should we review each year so the plan works?”

Your plan is a living thing. Each annual review, we update:

- Life changes: income, spending, upcoming goals.

- Key documents: wills, letters of wishes, beneficiaries, and LPAs (so everything still matches your intentions).

- Assumptions: inflation, returns, and timelines, so your model reflects reality as it evolves (no need to fixate on short-term moves).

How we build (and maintain) your model

- Capture today: income, spending, assets, liabilities, key dates and milestones.

- Map tomorrow: upcoming life events you expect (and ones you might choose).

- Agree assumptions: long-run inflation, returns and sensible buffers (kept simple and reviewed regularly).

- Test choices: retire earlier, work part-time, gift more, move house, see the impact instantly.

- Make the call: choose the path that balances freedom now with security later.

- Review your plan annually and update it as life changes.

Ready to explore your options?

Building your plan is the first step; the real value comes from proactively maintaining it as your life changes. If you’d like to explore what the future could hold for your finances and the choices you can make today, book a free, no-obligation chat, and we’ll take it from there.

If you need advice, we’re here to help. Schedule a free, no-obligation chat here. A guide on selecting a financial advisor is also available here.

This article is for general information only and does not constitute personal advice. If you’d like advice tailored to your specific circumstances, please contact us.