This month has some welcome positive news.

There was an increased likelihood of economic growth picking up in China as early as the second quarter. While economies are recovering in many parts of the world, they are a long way from where they would have been in the absence of Covid-19. Predictions are that global trade will continue to contract into the third quarter and start to rapidly recover after this.

There is an expectation that an eventual increase in the supply of goods as economies reopen will be met with weak private demand due to lost income and fears of Covid-19 transmission. As such, economists believe disinflation, a slowing in the rate of inflation, is likely to prevail in the medium term.

Economists expect central banks to keep monetary policy accommodative for the foreseeable future as economies face contraction and job losses as inflation is not an immediate threat.

The first quarter of 2020, or more accurately the second half of the first quarter, was a turbulent time for investors. The second quarter has seen a strong bounce back. There are a few points to pick out from the rosy picture of Q2:

Markets are still down from the start of the year. There is an easy mathematical error to slip into here as a market that has suffered a 20% fall needs a 25% rise (1/0.8 -1) to get back to square one. The S&P 500 gives a good example: it fell by 21.2% in the first quarter, but the 21.8% rise in the second quarter still leaves it down 4.0% on the year to date.

The UK market has seen a weaker recovery than most other markets, which may reflect the country’s response to the pandemic and, lingering in the background, the final Brexit deadline. The more domestically oriented FTSE 250 rose faster than its FTSE 100 counterpart. Nevertheless, the FTSE 250 is still down 21.8% from the start of the year, whereas the FTSE 100 has declined by 18.2%.

The gap between the FTSE 350 Higher Yield and FTSE 350 Lower Yield performance underlines what a relatively bad quarter value investing has experienced. ‘Higher yield’ is not good news when the focus is on dividends being cut or suspended. The implied historic dividend on the FTSE 100 has dropped by an eighth over the last three months.

The best market performance for the year to date comes from China, which did not drop as sharply as other markets in Q1. Its performance has helped the MSCI Emerging Markets Index.

Bond yields have generally fallen slightly, with the UK seeing the largest drops. UK gilts now have negative yields running out to six years and 30-year yields (0.64%). These are very close to those of Japan.

One of the biggest rises was in the price of oil. Brent crude started the quarter at $26.37 a barrel, while it ended June with a 58% increase.

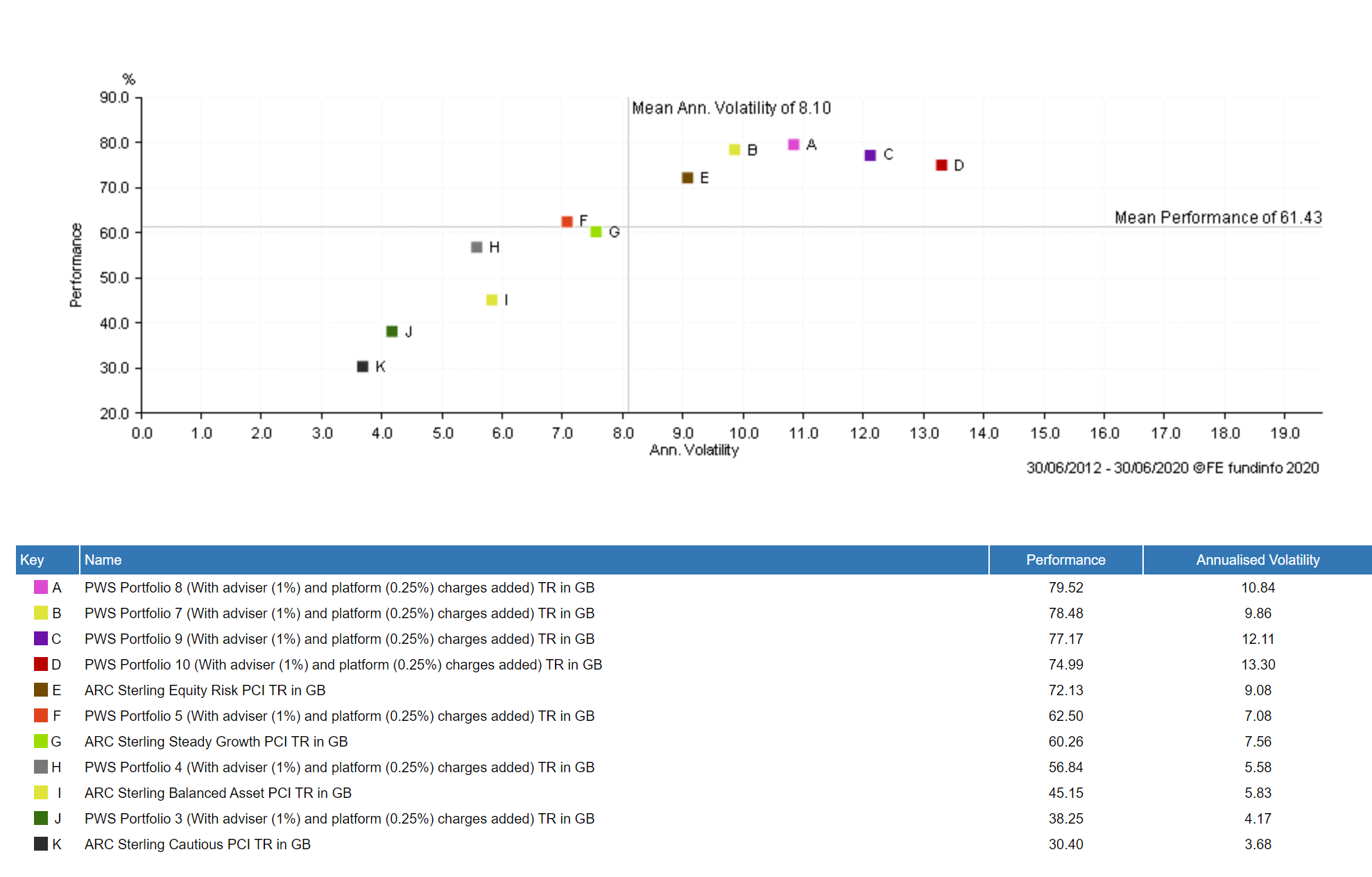

How have our portfolios done?

Our portfolios focus far more on the longer-term view than the shorter term. They don’t ignore it but we focus far more on managing risk than we do reaching for returns. Our portfolios are now more than 8 years old and have been getting to the point where they have gone through a full market cycle. As you can see below, they have outperformed the average wealth manager over 8 years:

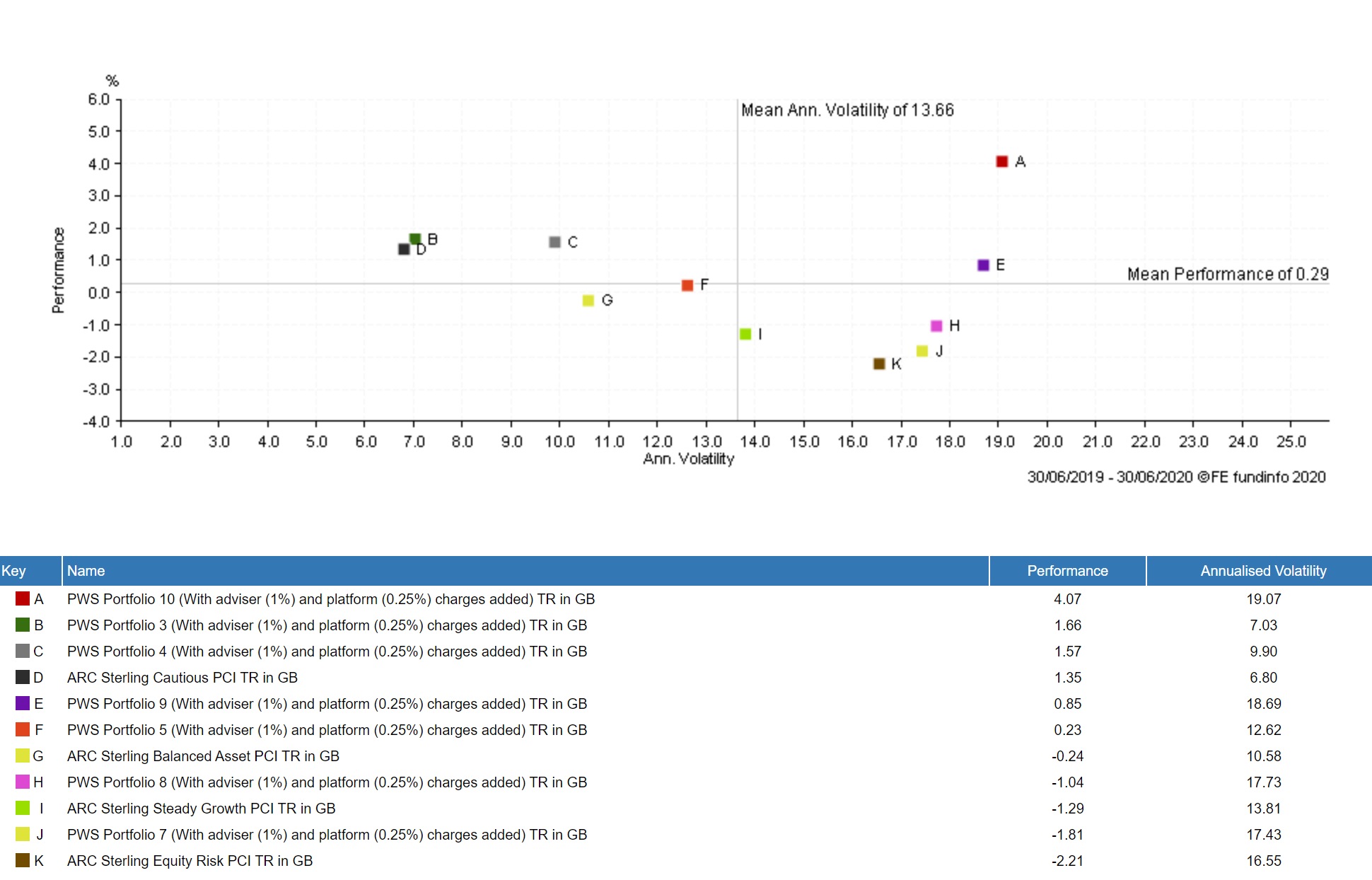

Over the last year this has also broadly been the case:

This won’t always be the case. We stick to a set level of risk and refrain from trying to time the markets. Over the short term, this may lead to underperformance. Over the long term, our investment process should help our clients get suitable returns.

Be aware that past performance is not an indicator of future returns and markets can go down as well as up.